“Welcome to Lake Wobegon, where all the women are strong, all the men are good-looking, and all the children are above average.”

- Garrison Keillor, News from Lake Wobegon - A Prairie Home Companion

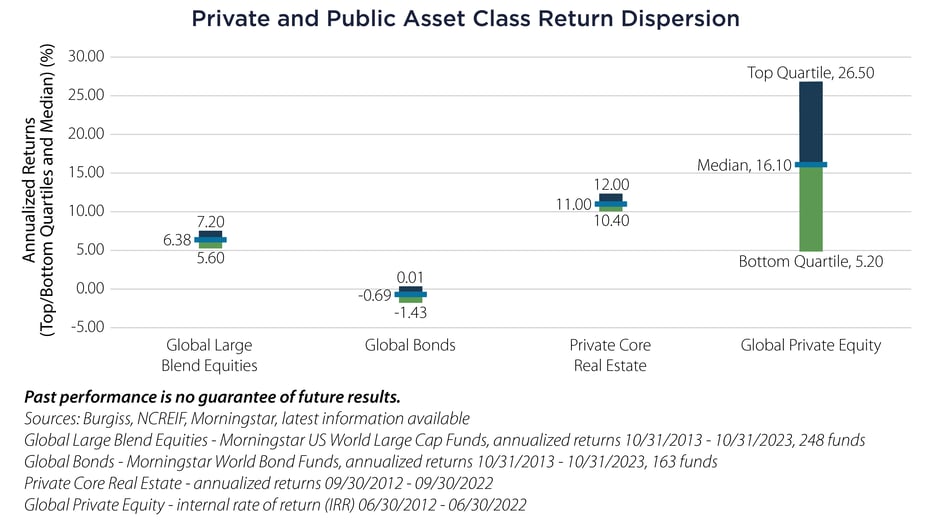

Dispersion of Returns

Private equity, at least according to headline numbers, provides compelling risk-adjusted returns when compared to public markets. Looking more closely, one stark contrast between public and private markets is the dispersion of returns between top and bottom quartile managers. The nearby chart illustrates that the top-bottom quartile dispersion for public market funds (both equities and bonds) is less than 200 basis points (bps), while global private equity is 2,000+ bps.

With such a wide performance dispersion, it is almost misleading to use “average” returns when describing private equity performance. While some investors benefitted greatly from an allocation, a significant cohort of investors experienced dramatic underperformance.

Private equity investors are allocating to an illiquid asset class with 10+-year investment horizons, with little optionality for changes once committed. An allocation to an underperforming manager can be an expensive mistake and difficult to “undo”, decreasing the likelihood that an investor achieves desired objectives.

Clearly, unlike the children of Lake Wobegon, not all private equity managers are above average.

A Changing Environment

When we last discussed private equity, we noted that over the past two decades, nearly ideal conditions for private equity outperformance were present; namely historically low financing costs, relatively cheap acquisition costs, coupled with robust initial public offering (IPO) and mergers and acquisitions (M&A) environments.

We also highlighted that these Goldilocks conditions were rapidly changing, with significantly higher financing costs due to higher interest rates, higher acquisition costs and a slowing IPO/M&A environment, indicating that private equity outperformance was unlikely to persist.

Given the changing environment for private equity and performance dispersion, the implications for investors are significant:

- Manager selection is paramount – a wide performance dispersion indicates that manager selection, rather than asset allocation, is critical for compelling risk-adjusted returns. Manager skill, resources and experience continue to play significant roles in fund performance.

- Adverse selection impacts can be material – an allocation to a private equity manager that provides bottom quartile performance (when expectations were median) creates 1,000+ bps return deficit while underperforming public equities.

- Limited optionality - private markets are illiquid, so it is difficult and expensive to reallocate capital from underperforming investments.

- Diversification is crucial but difficult to implement - illiquidity, manager access limitations, a limited size of allocation and a lack of transparency creates significant barriers for diversified exposure to private equity.

With weakening conditions, there is some likelihood that this dispersion could increase, perhaps dramatically, with manager and strategy selection becoming even more crucial for achieving investor objectives.

Beware the “Lake Wobegon effect” for private equity – for not all managers are above average.

Important Disclosures & Definitions

Basis Point (bps): a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument.

AAI000588 12/05/2024