In 2023, investors flocked to cash and short-term treasuries (the “T-bill and Chill” strategy) as these instruments outperformed core bonds, as measured by the intermediate duration Bloomberg US Aggregate Bond Index (US Agg), for most of the year.

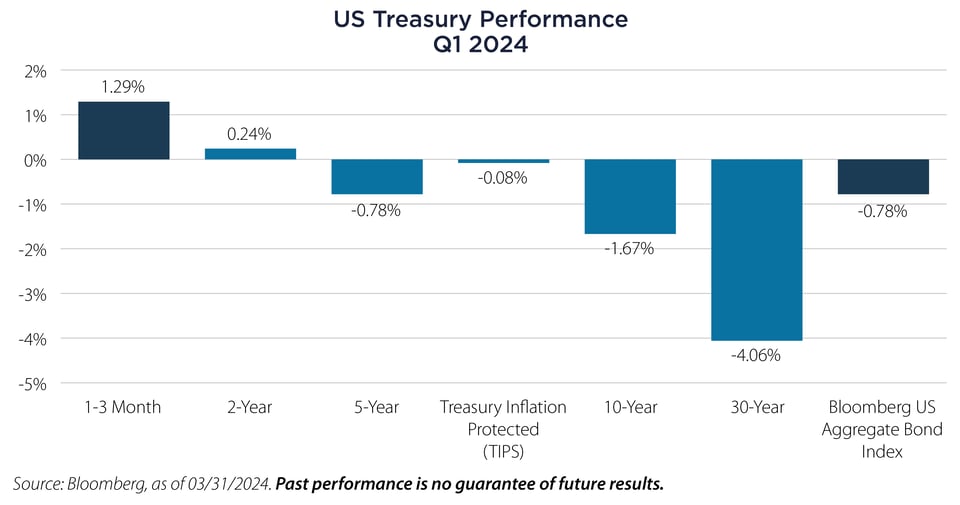

The current situation is somewhat similar, as longer term fixed income yields are moving higher resulting in a negative 78 basis point (bps) loss for the US Agg in Q1 2024.

Within a broader asset allocation framework, however, this strategy proved costly in 2023. Cash equivalents significantly underperformed equities, and even trailed behind Core and Core+ Bond categories by the end of the year.

This underperformance risk (or cash drag) persists for goal-oriented investors in 2024, as a similar scenario could unfold, particularly if the Federal Reserve (Fed) cuts rates.

The Market is Providing Investors an Additional Opportunity

The recent yield increases present an opportunity for investors parked in cash to balance their fixed income allocations along a flatter yield curve. For example, allocating to Core Bond funds now, amidst the yield uptick, may provide investors the potential to maintain yield levels while providing some downside protection from the potential for possible rate drops, equity declines or economic downturns. These events could occur independently in a "soft landing" scenario.

Attractive Points for Entry

A colleague's wall sign - "Make Your Move Before the Market Forces You To” - reminds us of the potential outcome when popular trades become too crowded. With record sums parked in cash equivalents, there's a looming demand for higher yields once the Fed cuts rates.

This influx of cash, referred to as the "Cash Trap," could drive up prices for higher-yielding assets, potentially causing a drag on overall performance for those who remain in short-term investments for too long.

Conclusion

Holding cash and short-term treasuries remains prudent in this environment, but should be viewed as a potential tactical risk reducer vs. a long-term replacement for a traditional fixed income asset sleeve (comprised potentially of government, corporate, securitized and municipal bonds, among others) within a broader asset allocation framework.

Despite the current attractiveness of short term rates, the opportunity costs of maintaining this strategy could be significant over time. The "T-bill and Chill" trade, driven by the fear of avoiding losses, overlooks long-term asset allocation principles which we believe are essential for achieving certain goals, like retirement.

While venturing into longer-duration assets (e.g., Core Bond funds) during rising rate environments may seem contrarian, recent trends suggest increasing investor interest in taxable and municipal bond funds.

This shift may indicate a thawing out to the potential for better fixed income returns in the future.

Important Disclosures & Definitions

Basis Point (bps): a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument.

Bloomberg US Aggregate Bond Index: a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, fixed-rate agency MBS, ABS and CMBS (agency and non-agency). One may not invest directly in an index.

AAI000673 04/09/2025