Many months of discussions with friends, family and colleagues regarding remote work inspired me to write this short ode to illustrate my take on the prevailing mindset of remote workers who, up to this point, have disregarded virtually all of the “return to office” memos from management.

An Ode to Remote Workers

In cubicles silent, once bustles of activity, now echo the ghosts of past creativity.

For out in the world, where the sunlight does dance, are the workers who won't give the office a chance.

No constraints in latitude, with their laptops in tow, in parks and cafes where their artistry flows.

Hot yoga in the boardroom couldn’t tempt them to stay, for they've found liberation in their own unique way.

Snacks, lunches and beer – gratis! And all on display, yet they savor their freedom, come what may.

For their office is anywhere they choose to roam, where creativity blossoms and privilege finds home.

No commutes to endure, no traffic's relentless chime, time is theirs to seize, in this liberated paradigm.

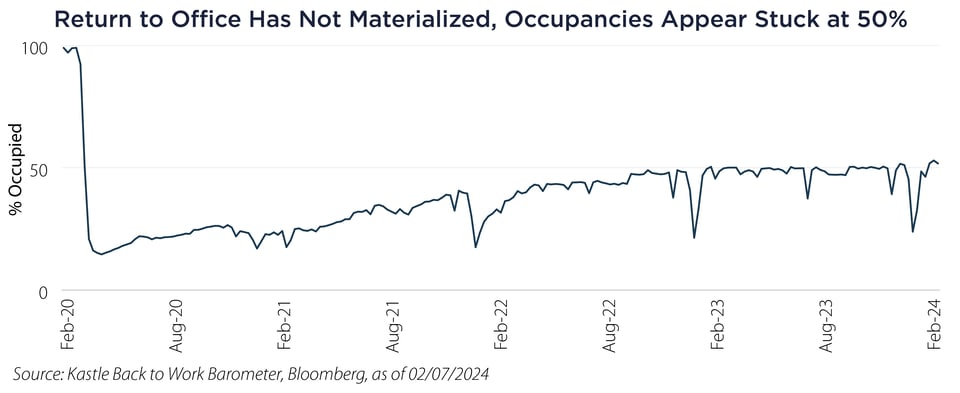

If the return to office was going to happen, as we were told it was “inevitable” numerous times in popular and business media over the past year, we certainly would have seen some evidence in the data by now. Yet, as illustrated nearby, despite both “carrot” and “stick” incentives from employers, office occupancy in the US has been stuck at 50% for past the 18 months.

Highest and Best Use

The grim realities of high vacancies, falling asset values and higher-cost debt refinancing are now front and center for many commercial office real estate owners, as well as significant real estate lenders such as regional banks, and large asset allocators such as pension funds, foundations and family offices. Still, the massive implicit discounts have yet to be effectuated in the carrying values for these assets.

When prevailing asset valuations appear to be out of whack, investors typically employ highest and best use1 economic principals to more broadly understand fundamental values. Unfortunately, there are very few alternative uses for 20-story vacant office buildings in second- and third-tier US cities. Except in rare instances, office buildings cannot be economically converted to residential or other uses. Clearly, office real estate owners’ face dramatic mark downs – in some cases, all the way down to vacant land values.

Other Attractive Real Estate Opportunities

It appears that the genie is out of the bottle for remote workers as they have too much to lose from flexible remote work arrangements and reduced commute times and expenses. They are unlikely to return to offices as expected, and vacancies are likely to stabilize at current levels.

Thus, we anticipate a rocky path for office real estate over the next 18-24 months or more as re-valuation, debt refinancing and balance sheet restructuring efforts ensue.

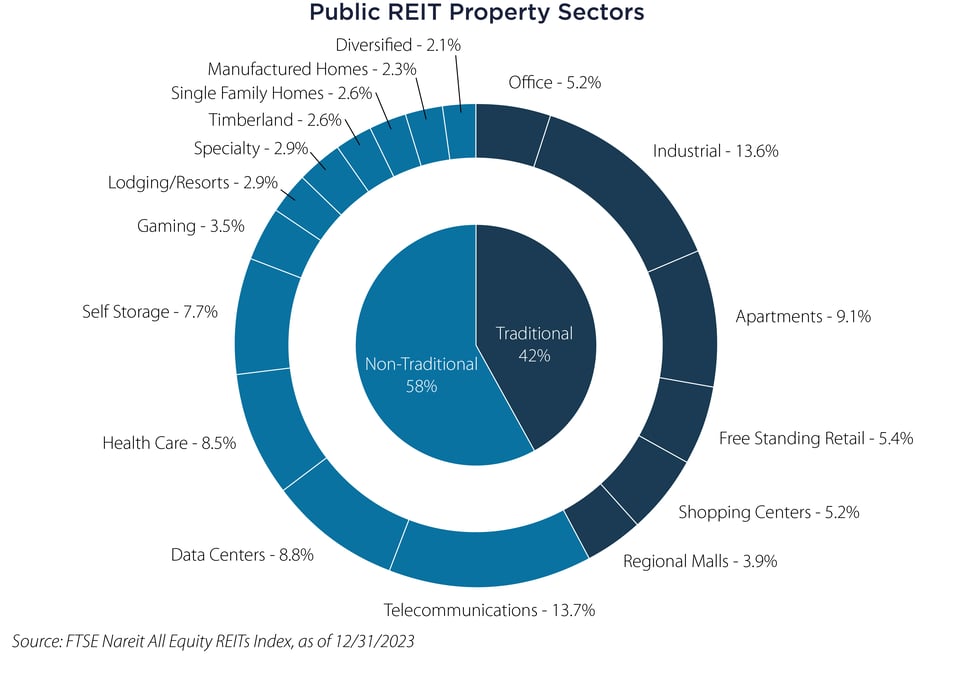

Despite the gloom over the prospects for office real estate, which represents only 5% by market cap of the public REIT universe2, we remind investors that real estate is a broad heterogeneous asset class with exposure to a number of different economic drivers and business models.

There are several promising secular themes in real estate sectors such as data centers, industrial warehouses, single family housing and higher-end malls that provide investors with attractive income and growth prospects.

We also note that active management has historically provided value for real estate investors, consistently outperforming the Morningstar category benchmark in both 5-year, and 10-year time frames.3

Important Disclosures & Definitions

1 Highest and Best Use: the Appraisal Institute defines highest and best use as “the reasonably probable and legal use of vacant land or an improved property that is physically possible, appropriately supported, financially feasible and that results in the highest value.” Appraisers typically apply these four tests to determine that use.

2 Source: NAREIT, as of 12/31/2023

3 Source: SS&C ALPS Advisors, Morningstar Real Estate Fund Category Analysis, as of 12/31/2023

FTSE NAREIT All Equity REITs Index: a free-float adjusted, market capitalization-weighted index of US equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property. One may not invest directly in an index.

Kastle Back to Work Barometer: a measure of current average weekly (first time a day) swipe activity across a 10-city sample of commercial office buildings which utilize Kastle building security, compared to a weekly average from before office use dropped due to COVID-19. The 10-city sample includes: Houston, Chicago, Austin, New York, Dallas, Los Angeles, San Francisco, Washington D.C., San Jose and Philadelphia.

AAI000628 02/20/2025