Gold receives lots of attention during times of market stress, and given our recent focus on all the uncertainty in the market, we thought the idea was worth a closer look.

We have previously pointed out that cryptocurrencies only derive value from people believing that they’re valuable. There isn’t anything really intrinsically valuable about cryptocurrencies, like a right to receive fixed interest payments or a residual claim on assets.

Gold can be reasonably placed into a similar camp. While there are some broad commercial applications for gold, such as jewelry, its historical use as a method of payment died with the gold standard in 1971.1 Today, the primary driver of gold’s value is the near-unanimous opinion that gold is valuable.

But there is one big difference

The difference is who exactly believes that gold is valuable. In the case of bitcoin and similar cryptocurrencies, a lot of the support comes from an anti-government, anti-establishment ideology. The decentralization and lack of oversight by a regulatory body is hailed as a key feature of the system. Unfortunately, this is exactly why the space is riddled with theft and fraud, and why these coins remain a risky, speculative gamble.

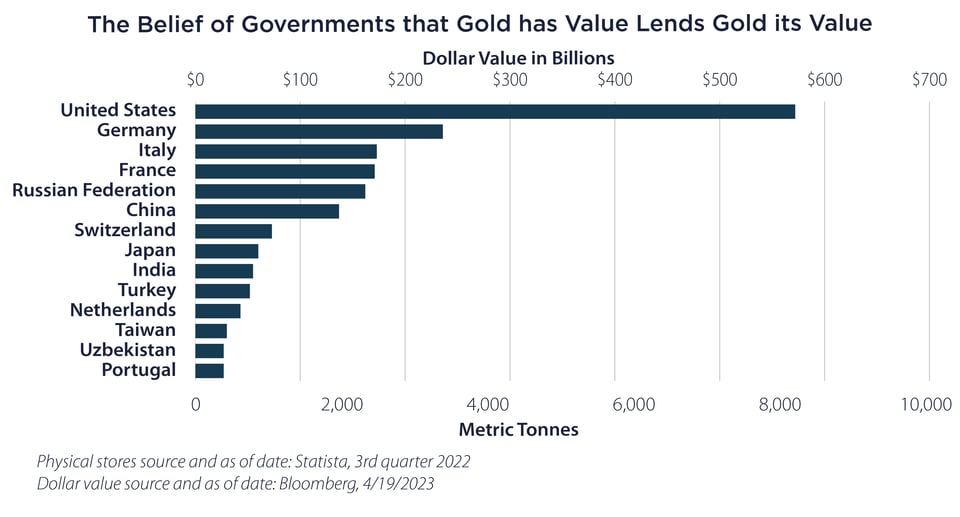

The history of gold as a method of payment sets it apart. Not only does gold hold a favored place in our prefrontal cortexes as a symbol of money and wealth, it also holds a favored place in the vaults of all the world’s major governments. This lends gold significant credibility as a reliable store of value. The same thing would occur if governments (more reliable ones than El Salvador) start hoarding bitcoin.

Gold performance during market shock

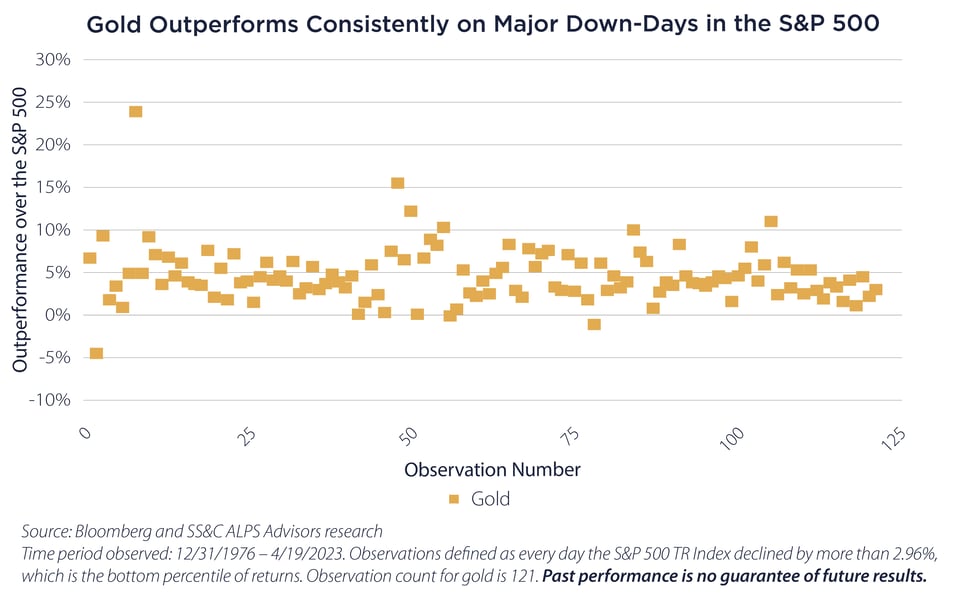

Given the lack of fundamentals to drive prices, we must conclude investor psychology is nearly entirely responsible for price fluctuations. Because one of gold’s main claims to fame is its nature as a “safe haven” asset—one that will protect the investor in a market decline—we decided to look at the performance of gold when the S&P 500 Index experienced a significant down day.

We looked at the bottom percentile of single-day returns on the S&P 500 since 1976, which is a return ceiling of about -3%. On the 121 days on which the S&P 500 returned worse than -3%, the average return for the S&P is -4.5% and the average return for gold is 0.2%.

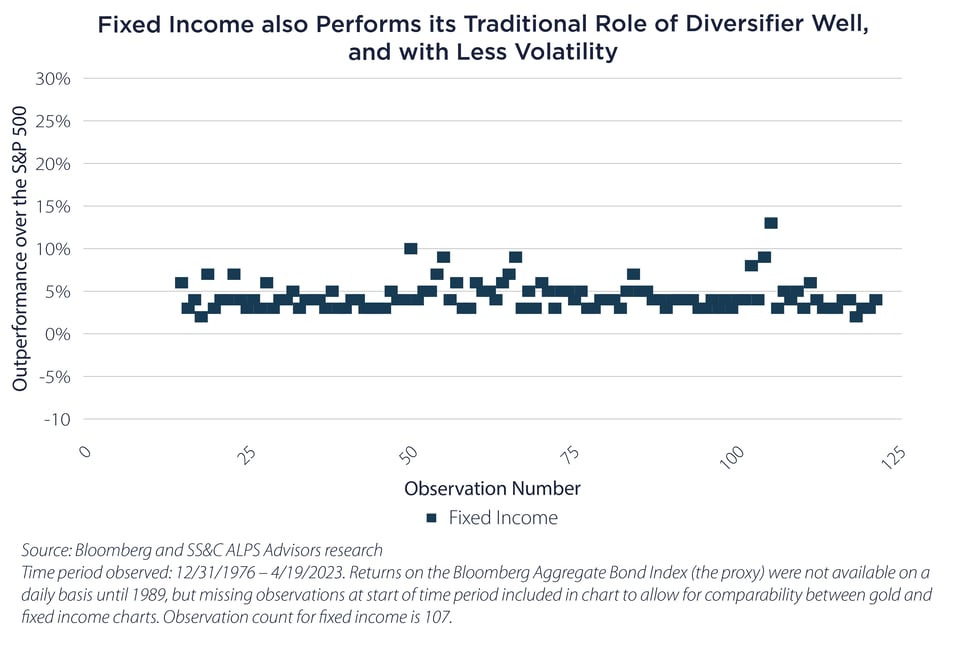

Astute observers may have noticed achieving an almost 0% absolute return isn’t really that exciting, and one might wonder if the S&P’s more traditional diversifier asset couldn’t perform the same function. Fixed income, as measured by the Bloomberg US Aggregate Bond Index, performed similarly to gold, averaging 0.1% returns on down days in the S&P.2

Is anything different this time?

Gold’s hype may be reaching new levels, as Russia’s war in Ukraine and the resulting weaponization of the US dollar to punish Russia has led to concerns about de-dollarization. A possible side effect of this could be renewed interest by governments in gold, as it would be much more difficult for the US and her allies to control, but wouldn’t require the establishment of an entirely new monetary regime.

A possible black mark against fixed income in the current environment is the Federal Reserve’s insistence that interest rates will stay higher for longer. This implies fixed income may lose some of its appeal, as falling rates (or anticipation of the same) are the saving grace that lifts fixed income prices. Currently, the fixed income market does not believe this to be the case, with several rate cuts already expected by the end of the year. However, if those cuts don’t materialize, even in the face of a recession, gold could end up as a standout asset.

While we aren’t entirely convinced of either of these scenarios, we have noted that we are in a uniquely uncertain time. There are other factors to consider, including gold’s performance around recessions and its correlations to the other asset classes. But given that uncertainty itself drives interest in safe haven assets such as gold, we are becoming increasingly interested in its role as a diversifying asset in a world where downside risks abound.

Important Disclosures & Definitions

1 This was really just the last nail in the coffin. By this point gold wasn’t being used to buy milk at the grocery store, but the price for gold was guaranteed by the US government. So you could buy your milk or a certain, consistent amount of gold from the government.

2 The time period observed for fixed income returns is smaller, beginning in 1989 instead of 1976. Daily returns for the Bloomberg Aggregate Bond Index are not available on a daily basis prior to 1989.

Bloomberg US Aggregate Bond Index: a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, fixed-rate agency MBS, ABS and CMBS (agency and non-agency).

S&P 500 Index: widely regarded as the best single gauge of large-cap US equities. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

One may not invest directly in an index.

Performance data quoted represents past performance. Past performance is no guarantee of future results; current performance may be higher or lower than performance quoted.

AAI000261